Why are experts hedging copper price bets?

)

As India is a minor producer of copper ore, with no significant occurrences of the metal in the mineral, the two major smelters in the private sector are run with copper concentrate of foreign origin. In 2010, the Indian Bureau of Mines estimated the country's ore reserves in metal terms at 4.8 million tonnes (mt) and resources at 12.3 mt. As is the case with all other minerals from iron ore to bauxite, a palpable lack of urgency marks our attempts to convert copper ore resources into reserves.

Currently, domestic concentrate production accounts for only about four per cent of the requirements of the three smelters here, including government-owned Hindustan Copper Ltd (HCL)'s modest-sized one. Hopefully, in the next five years, HCL will be able to increase ore production to 12.4 mt, against 3.657 mt in 2012-13, by expanding operating mines and restarting those closed earlier, in most cases thoughtlessly. The enhanced mines production won't, however, reduce the country's copper concentrate import dependence, as the local custom smelting capacity without mines linkages is set to rise in the next few years.

The Vedanta group is set to double its copper smelting capacity at Tuticorin in Tamil Nadu. Together, Hindalco and Vedanta account for about 80 per cent of the local primary copper market. The rest of the demand is met through HCL and imports, made easier in the last couple of years by low prices. Except for about eight per cent concentrate the Tuticorin smelter gets from group-owned mines in Tasmania, Australia, it, along with Hindalco's Bharuch smelter, buys the feedstock from third-party suppliers at the London Metal Exchange price, after deducting treatment and refining charges (TRCs).

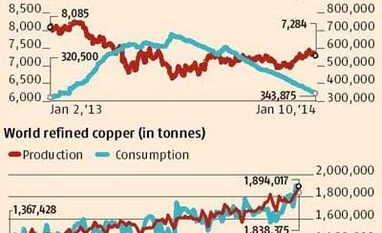

There is good news for custom smelters. According to Swiss financial services group UBS AG, TRCs could rise 29 per cent this year, principally aided by mines production increases. International Copper Study Group predicts a 6.4 per cent rise in mines output this year. Globally, the ten major mines expansions alone will increase concentrate supply by about one mt. Red metal prices will remain under pressure, as refined global copper production is set to rise about 10 per cent to about 22 mt in 2014.

In a repeat of what happened last year, firm TRCs with spot charges at multi-year highs will encourage custom smelters to make full use of their capacity. Smelters benefit from high TRCs when the market doesn't favour copper. The opposite happens in a bull market, when smelters have to settle for low TRCs. China, the world's largest producer of copper, found in ruling TRCs a major incentive to smelt as much as 6.23 mt of copper in the 11 months ended November 2013. That country, which accounts for 40 per cent of global consumption of the red metal, is said to be importing over one mt of concentrate a month to feed an ever-expanding smelting capacity.

Generally, copper prices reflect the health of the world economy. This was much in evidence in 2013, when copper first moved out of positive territory on concern about a slowdown in Chinese manufacturing, a cash crunch and speculation about the rate at which the US Federal Reserve would wind down stimulus efforts. The market sentiment was further worsened by increased supplies from leading resources groups that were largely spared production dislocations, either by accidents in mines or labour agitations. Even while copper prices fell seven per cent in 2013, the metal scored its most impressive monthly gain of about four per cent in December, compared to September 2012.

Hopes of a deepening US recovery-bull operators have seen the US Fed's scaling back of monthly bond purchases by $10 billion as confirmation of an economic turnaround-and the purchasing manager's index (PMI) for Euro zone at a 31-month high of 52.7 in December will explain copper's good performance last month and New Year's first trading session on the comex division of New York Mercantile Exchange. As the copper market is news-sensitive, the sentiment was blighted by Beijing's official PMI sliding from 51.4 in November to 51 last month. Official admission that decline in China's growth, which started two years ago, is likely to continue through this year is yet another damper for the market.

So, what is the copper price outlook? Instead of making any firm forecast, experts are playing it safe. One group isn't sure if the super cycle in commodities has come to an end. So, there could be scope for copper prices to rise. At the same time, many are questioning if growth in Euro zone, the third-largest market for the metal after China and the US, will be maintained.

This will explain why so many are hedging their copper bets. As Bank of America Merrill Lynch says, "We believe copper is not too hot and not too cold. Next year's average may be close to quotations this year." But like gold, copper is not finding favour with Goldman Sachs, which wants investors to give more attention to stocks than commodities.

Don't miss the most important news and views of the day. Get them on our Telegram channel

First Published: Jan 13 2014 | 10:33 PM IST