)

Prices of base metals have seen some recovery in the past week, after most of these visited their two-six year lows, following the Greece crisis and sharp fall in the Chinese equity market. However, things are stabilising and the Iran nuclear deal has given further relief to the markets.

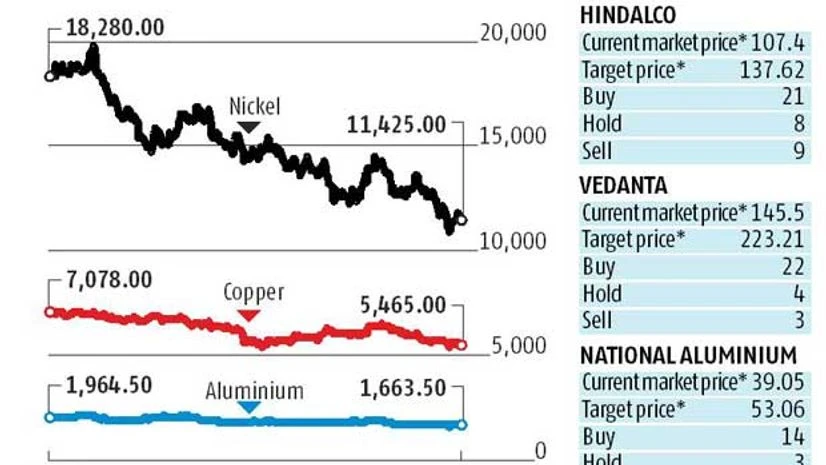

While aluminium, copper, nickel and tin fell to six-year lows last week, zinc has bounced from a 22-month low and lead from a five-year low. But, prices are still lower six-eight per cent compared to the beginning of the financial year. Industry experts, however, believe the worst for base metals is over and prices would gradually start moving up. And, this is a good time for metal consumers to lock their future requirements, and long-term investors to start accumulating integrated metal producing companies.

The Chinese economy is undergoing major structural changes, away from an unsustainable model based around investment in heavy industries towards a more sustainable growth model, based on consumption. This means slower growth in demand for industrial metals in the interim. This has been reflected in the realisation that Chinese demand for steel had peaked and prices had collapsed to multi-year lows.

Recognising these risks, Chinese authorities had taken necessary steps to support economic activity in order to achieve their seven per cent annual growth target.

Despite the fact that China faces some major economic challenges, "it would be dangerous to think that the authorities have suddenly become impotent in their efforts to support economic growth," said Nic Brown, head of research at Natixis Commodities.

Some impact is already seen. In the real estate market, prices are beginning to rise again after a period of stagnation. Inventory of unsold floor-space is falling.

Fears of Greece exiting from the euro zone is also tapering, which, along with a weakening euro and low commodity prices, provide opportunity for rapid economic growth in the region.

So far, weak base metal prices have impacted a profitability of non-ferrous players. Hindalco's US subsidiary, Novelis, was not able to pass on costs of earlier metal purchases that it bought at higher regional premiums. For its Indian operations, volume benefits coming from expanded capacities at the Aditya and Mahan smelters are getting diluted due to weak aluminium prices, while profitability is under pressure, as with expansions completed interest and depreciation costs are increasing. Hindalco's margins and profits are expected to remain under pressure in the June'15 quarter too.

For Vedanta, the situation is not different and is compounded by the bearish trend in crude oil prices and power realisations. For the quarter ending June, analysts at Motilal Oswal Securities expect a 24 per cent year-on-year decline in Vedanta's consolidated Ebitda (earnings before interest, tax, depreciation and amortisation) despite higher profitability in copper and zinc businesses providing some cushion. The merger with cash-rich Cairn India would lead to substantial reduction in Vedanta's debt.

Nalco's, the state-owned aluminium/alumina player, problems are compounded by dependence on external coal for its power plants. Analysts expect a 19 per cent rise in aluminium production and six-seven per cent increase in alumina production in FY16. But, with low realisations, sales are seen growing marginally and profits estimated to decline.

The scenario, however, might change for the better if prices move up. One thing though is quite clear. The concerns seem priced in stock valuations. With metal prices seen recovering at a slow pace, it might be sometime before analysts start factoring them in their estimates. But, their price targets for the stocks (see table) suggests there is upside from current levels.

Experts also have an interesting suggestion for consuming companies, and that is to start locking their raw materials needs at these lower levels.

"We have already seen some forwad thinking with European companies looking to lock in attractive raw material costs to support expanding order-books in the years ahead, which suggests outlook for Europe is quite positive," said Brown.

"Small and medium-size companies using base metals as raw materials and other consumers should start buying metals now. If they can afford it, buy physical commodities or hedge their future requirements at current prices," said Gnanasekar Thiagarajan, research director, Commtrendz, a risk advisory firm. He also says power transmission companies that use copper and aluminium should consider this.