)

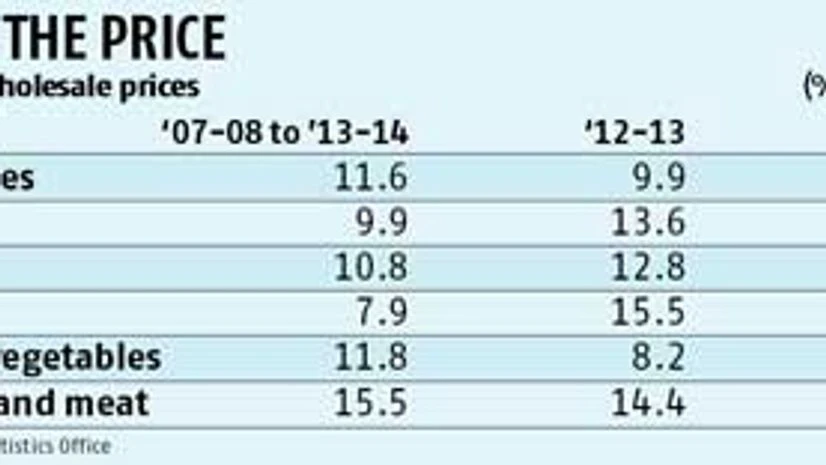

Inflation in India is generally triggered and led by food price inflation. This is easily seen from the fact that most inflationary episodes witnessed rising relative price of food. The current inflationary episode, which began in 2008-09 and still continues, is no exception. In the period since 2007-08, the average year-on-year inflation, as measured by the wholesale price index (WPI), has been 7.3 per cent, while the average year-on-year food inflation has been 11.6 per cent. The same features are reflected in the fact that CPI-inflation, inflation measured by the consumer price index (CPI), is usually higher than WPI-inflation; food has a higher weight in CPI than in WPI. In the period April 2012-March 2014, the average year-on-year WPI-inflation was 6.7 per cent, while the CPI-inflation was 9.9 per cent.

Why does inflation tend to be led by food price inflation? The short answer is that, in India, there has been and still is a food constraint on economic growth. Given the production conditions in agriculture, growth of food production tends to be slow. Because food figures prominently in the consumption basket, any rate of growth of incomes implies a corresponding rate of growth of demand for food. Hence, given the feasible growth of food production, there is a certain "ceiling" rate of growth of gross domestic product (GDP), which keeps the demand for and supply of food in balance. Whenever the actual rate of growth of GDP exceeds this "ceiling" rate - and this has happened many times - food prices rise and inflationary pressure is generated.

Mismatch between GDP growth and growth of food production has certainly been a factor in the current inflationary episode. While during 2002/3-2007/08, a GDP growth rate of 8.7 per cent had been associated with an agricultural growth rate of 4.8 per cent, in the period since 2007/08, a GDP growth rate of 7.2 per cent was associated with an agricultural growth rate of only 2.8 per cent. The stimulus package introduced in the wake of the global financial crisis of 2007/08 did succeed in maintaining high GDP growth, but also generated food price inflation as agricultural growth faltered.

But there is something more to the story. With rising incomes, food consumption patterns have been shifting; the share of cereals in average food consumption has been declining while the shares of "fruit and vegetables" and "eggs, meat and fish" have been growing. In the current inflationary episode, therefore, we would have expected to see price rises being largely confined to "fruit and vegetables" and "eggs, meat and fish". In reality, however, prices of these items increased only slightly faster than the price of cereals, the increase in which was high. Particularly surprising is the fact that the prices of rice and wheat have been recording large increases.

Why have the prices of rice and wheat been rising nearly as fast as the prices of "fruit and vegetables" and "eggs, fish and meat"? The answer is: because of the peculiar system of price support and procurement in place. For a long time now, there has been open-ended procurement of rice and wheat at what are still misleadingly called minimum support prices (MSPs), though MSPs have been no different from procurement prices since the mid-1970s. This means that wholesale market prices cannot generally fall below MSPs, so that growth of the latter effectively determines the growth of the former. During 2007/08-2013/14, MSPs were increased, on average, by 9.9 per cent for rice and 5.8 per cent for wheat. The actual average increases in wholesale prices - 10.8 per cent for rice and 7.9 per cent for wheat - were pretty close. And while prices were rising fast, the government was carrying, throughout 2008/09-2013/14, average stocks of 30 million tonnes of rice and 18 million tonnes of wheat.

So, at least in the case of cereals, price rises had much to do with the government's policy of rapidly increasing MSPs combined with open-ended procurement. Arguably, moreover, this policy also contributed to increasing the prices of higher-value agricultural products by pre-empting reallocation of land and other resources from cereals to these products. Thus, inflation since 2007/08 has been fuelled not just by demand pressures generated by the mismatch between GDP growth and agricultural growth, but also by the existing system of price support and procurement.

Taming food price inflation clearly requires removing the mismatch between agricultural growth and GDP growth. And that means achieving acceleration in agricultural growth. In the short-run, however, it is GDP growth that has to be lowered. Arguments such as that the Reserve Bank of India (RBI)'s policy of maintaining high interest rate hurts growth but does not bring down inflation or that the fiscal deficit needs to be lowered miss the point. Lower GDP growth is actually needed. And reducing the fiscal deficit will hurt GDP growth just as maintenance of a high interest rate will.

However, the maintenance of high interest rate has disadvantages. It encourages inflow of foreign institutional investment, which causes exchange-rate appreciation and forces RBI to sterilise much of the inflow and thus accumulate foreign currency reserves. For this reason, a combination of lower interest rate and a lower fiscal deficit is a better policy mix.

Restraining GDP growth, however, will not be sufficient to bring down food price inflation if the current system of price support and procurement remains in place. Radical reform is required in this area. The objective of intervention in the cereals market should be to maintain price stability, that is, maintenance of price within a narrow band. The lower bound of this band should guarantee a small profit for cereal producers, while the upper bound is to be defined with consumers' interest in view. In a good crop year, when the market price threatens to fall below the lower bound, the government should prevent this through procurement. In a bad crop year, when the market price threatens to rise above the upper bound, the government should prevent this through public distribution.

The writer is honorary professor at the Institute for Human Development, New Delhi

Disclaimer: These are personal views of the writer. They do not necessarily reflect the opinion of www.business-standard.com or the Business Standard newspaper