)

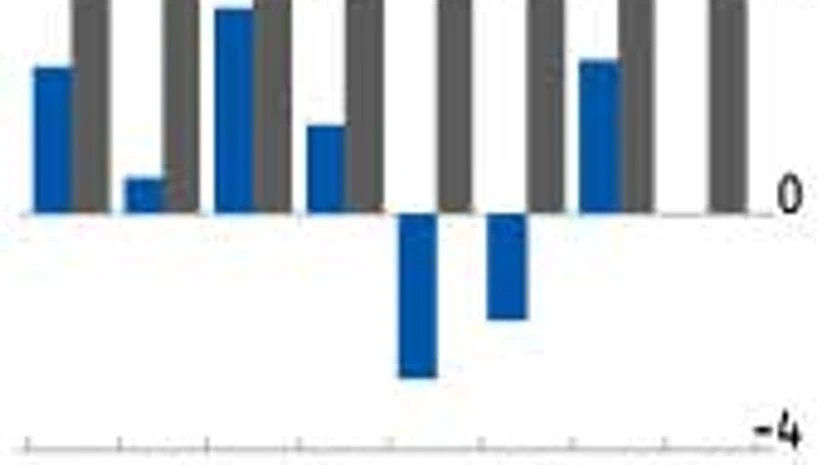

The sense of foreboding that had gripped investors a few months ago has faded. While the currency stability has largely contributed to this turnaround in sentiment, macroeconomic data points are also showing signs of improvement. With the trade deficit for September dipping to $6.76 billion from $18 billion last year, economists are already cutting their current account deficit estimates for FY14. Undoubtedly, the government's clamp-down on gold imports has helped bring down this deficit sharply.

Weak industrial growth has also led to relatively weaker oil and non-oil imports. Even if imports pick up in the second half of the year, the overall trade deficit might be lower by $10-20 billion in FY14. However, if mining issues are not resolved, then import of iron ore and coal could put push up the trade deficit again. Coal imports have risen from $1.19 billion in April to $1.42 billion in July.

Industrial production data shows mining continues to decline and this could stress the external sector if no resolution to the mining issue is found. But on the positive side, manufacturing and electricity are showing a pick-up over the past few months. Industrial production, too, is showing signs of a revival. Going by consensus estimates, the index for industrial production for August is expected to expand by two per cent. This uptick would be largely driven by a pick-up in manufacturing and electricity.

Religare's Tirthankar Patnaik expects electricity to grow by 6.4 per cent, year-on-year (y-o-y), and manufacturing by 2.4 per cent. Mining will continue to decline. Morgan Stanley says the delay in US Fed tapering and measures taken by the Reserve Bank of India (RBI) over the past few weeks have reduced the short-term funding risks for India. However, the structural problems of higher real rates and lower GDP growth still remain intact.

The other piece of data expected next week is wholesale price index (WPI) inflation figures for September. According to consensus estimates, WPI should come in at six per cent for the month and consumer price index at 9.6 per cent. While the rupee's depreciation is expected to push up the headline print, high vegetable prices would also play spoilsport. Given that inflation remains sticky, most economists believe the RBI's policy stance would definitely not be dovish.

Many economists are expecting repo rate hikes of 25-50 basis points (bps) spread over the next quarter. However, a sustained increase in rates is ruled out. While a majority of economists are not ruling out a one-off hike, few believe it would be a sustained trend. However, if RBI chooses the old-fashioned way to battle inflation, rate hikes could be imminent and that would negatively impact the banking sector as asset stress would increase.