)

In July 2007, Chuck Prince of Citigroup justified punters contributing to the build up of a huge financial bubble, when he said, "As long as the music is playing, you've got to get up and dance. We're still dancing." Six years later, traders still espouse the same philosophy for the same reasons.

One difference is that the current bubble has been deliberately created and it has a regulatory cut-off switch. Come September, the US Federal Reserve may tighten its Quantitative Easing Programme (QE3). If it does, traders will dump risky assets, like rupee debt and equity.

Alternatively, the Fed may let QE3 run at the same expansion rate, if targets in terms of US reflation and employment are not met. The latest statement by Fed Chairman Ben Bernanke suggests that he would like to let the Fed continue being "accommodative" but several of his colleagues are more hawkish.

One issue with "artificial bubbles" is that they create liquidity traps. Spearheaded by the Fed, most central banks have pumped out easy money. This has held interest rates low. But it hasn't stimulated economic growth as desired. Instead of investing in real activity, traders have parked excess cash in financial assets. Hence, bubbly asset values that contrast with low aggregate demand.

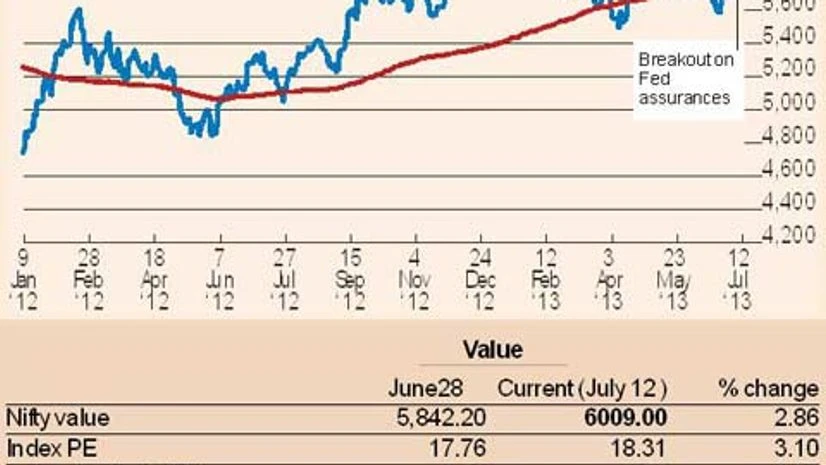

We've seen early warning signs in India of what could happen as the Fed cutbacks. In June, the foreign institutional investors (FIIs) sold over $7 billion in rupee assets and the dollar dipped to record levels in early July while the stock market slid.

Bernanke's statement led to a qualified change of stance with FIIs buying rupee equity worth Rs 645 crore last Friday. While the FIIs are net sellers in July, local operators have gone long betting that the change of attitude will last. In a thin market, this has pushed the Nifty past the 6,000-level.

The bubbly nature of Indian equity assets is marked with fundamentals and valuations looking distinctly out of line. The Q1, 2013-14 results season has kicked off. Infosys climbed 11 per cent on Friday after it declared lower sequential net profits, single-digit year-on-year earnings growth, flat operating margins and left FY2013-14 revenue estimates unchanged.

The 50-stock premier index is now traded at a trailing four-quarter price-to-earnings (P/E) of 18-plus. A report in this paper on July 8 (Profit boom amidst sales gloom) presented averaged estimates about Nifty Q1 earnings from seven brokerages. The consensus is a fall of 0.4 per cent in combined sales for the Nifty 50 (excluding Coal India), along with a rise of 11.8 per cent in net profits. Operating margins are expected to decline. Eleven of India's 50 largest companies are expected to see double-digit earning per share growth while as many as 26 are expected to see declining earnings or losses.

There seems to have been no revival in activity in Q1, going by the latest macroeconomic data. The Index of Industrial Production (IIP) shows 1.6 per cent year-on-year contraction in May 2014, and April 2014 IIP growth was revised down to 1.9 per cent from the preliminary 2.3 per cent.

Consumer inflation climbed in June 2013 to 9.9 per cent from 9.3 per cent in May, if one believes the Consumer Price Index. The Wholesale Price Index (WPI) numbers are expected on Monday and most analysts expect WPI to up by more than 5 per cent as well. Some of the rise may be attributed to the weaker rupee but food inflation also remains very high at 11-plus.

Private sector data suggests poor sentiment. Automobile sales contracted in June, for the eighth month in a row. The Purchasing Managers Index stood at 50.1 which is on the verge on contraction (50 equals to no change and below 50 is contraction).

Poor sentiment, high inflation, low or negative earnings, industrial contraction, etc., makes for an ugly picture, especially when one factors in the record current account deficit, the record fiscal deficit, and a very real chance of further deep currency depreciation and defaults on overseas corporate debt.

The Reserve Bank of India has a tricky task. Does it cut policy rates at end-July with due regard to the weak demand? Or, does it hold rates, or even raise them, for fear of inflation going out of control and the rupee spiralling down if FIIs continue to exit? The central bank will probably hold or hike because of the fear of a balance of payments crisis.

Against this backdrop can assets be reasonably valued at 18-plus P/E ? This will last, at best, only so long as the FIIs have loose change to spare. Since Q1 projections are low, as cited above, it's quite likely that some big companies will beat earnings consensus. We could well have a situation where valuations rise even further in the short term. This might enable long trades in the information technology sector and maybe, in other export-oriented industries.

Instead of squaring up to the structural issues that are so glaringly apparent, the government is trying palliative measures to induce further portfolio inflows. It is also trying to prevent Indians from hedging or speculating on the rupee weakening more. At the same time, measures like the Food Security Ordinance are likely to bloat the fiscal deficit even further.

In August, or September, or whenever the Fed cuts back, there is likely to be a serious crash in equity values. Unless the economy makes a miraculous turnaround of course, and maybe, even then. Until there's clarity on the Fed action, there's likely to be continuous volatility with big swings in either direction on temporary news flow. Holding deep puts on the Nifty at say, 5,500-level may be a good idea until September, at least. The pessimist could even make a case for long December 5,000 puts.

Disclaimer: These are personal views of the writer. They do not necessarily reflect the opinion of www.business-standard.com or the Business Standard newspaper