)

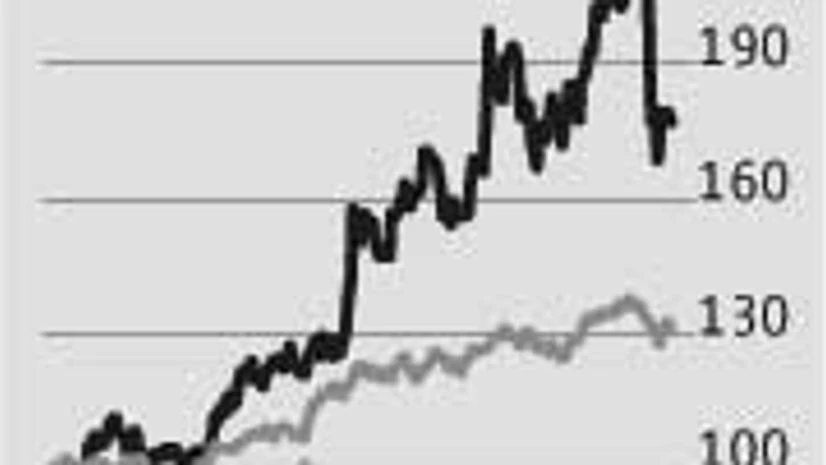

Despite expectations of a recovery in the economy, consumption trends are clearly showing signs of stress. Havells India, the electricals equipment major, which began the financial year with expectation of robust growth, has scaled down this estimate for FY15 from 17-20 per cent to 12-14 per cent. The market has reacted negatively, with the stock, which had gained 18 per cent in six months, shedding most of these gains in December.

The company has cited sluggish consumer spending and weak consumer sentiment as reasons.

The revised forecast is expected to put further pressure on valuations, which have run ahead of fundamentals.

Despite the fall in the stock, it is trading at 27 times its FY16 earnings estimate, significantly ahead of the historical multiple of 17 times, says PhillipCapital. The trading multiple is in line with trends in the fast-moving consumer goods sector.

Given Havells' weakening growth, the stock could come under further pressure.

Another negative is an increase in pension liabilities for its Sylvania in the second half of FY15, as bond yields have declined sharply, which will impact the company's profitability.

However, the revenue growth estimate for Sylvania is unchanged at three-five per cent.

Analysts say Havells' margins are expected to remain stable. For Sylvania, they expect operating profitability to improve.