"Mindtree: Valuations rich despite recent correction")

Following Mindtree’s growth warning on Friday, most analysts have trimmed their full-year revenue and earnings estimates and consequently, their target prices for the stock. Though the company management is confident of meeting Nasscom’s revenue growth estimate of 10-12 per cent this financial year, analysts are not convinced.

The latest move by analyst comes after the company said there are near-term headwinds in the form of project cancellations, slower ramp-up in large clients and continued weakness in its UK-based subsidiary— Bluefin, which would lead to a sequential decline in both constant currency revenues and margins in the September quarter.

The company also seems to be struggling with client-specific issues in banking, financial services and insurance (BFSI) and retails. Macro demand headwinds faced by the technology sector in the wake of uncertainties arising from Brexit, US elections, etc are some other monitorables. Europe accounts for 23 per cent of Mindtree’s revenues.

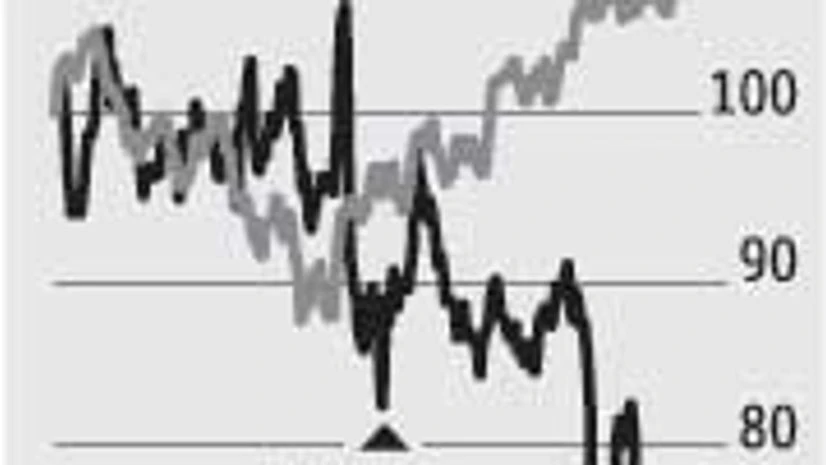

It is thus not surprising the stock fell five per cent on Tuesday. It hit a new 52-week low of Rs 504.5 intra-day before closing at Rs 521.70. This underperformance came on a day when both the Sensex and the BSE IT indices ended the day in green—Sensex was close to its 18-month high. This has only added to the Mindtree scrip’s under-performance all through the past year, during which the stock has fallen 20 per cent.

Notwithstanding these pressures and the toning down of estimates by analysts, the Mindtree scrip still trades at 17 times the FY17 estimated earnings. This is much ahead of its historical average one-year forward price to earnings ratio of about 12 times, and also higher than some of its larger peers. Given the weak near-term outlook, most analysts believe these valuations are difficult to sustain.

Analysts say Mindtree is a good company in the mid-cap IT space, given the healthy momentum it has witnessed in its digital business but it needs to address the above-mentioned issues for sentiments to improve.