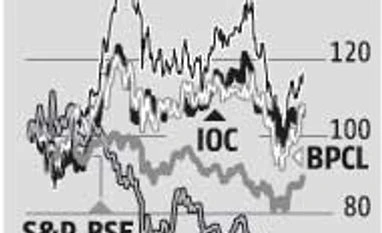

Oil PSUs making the right moves

Good timing of assets' buy; fuel rate raise to up gross margins in line with medium-term averages

"Oil PSUs making the right moves")

The purchase of stakes in Russia’s oilfields by public sector undertakings (PSUs), increase in fuel price by oil marketing companies (OMCs) and the Petroleum And Natural Gas Regulatory Board’s rate revision for GAIL’s KG (Krishna-Godavari) pipeline are positives for PSU oil companies.

First, in the current environment when oil and gas prices are subdued, assets are typically available at reasonable valuations.

Consider this: Indian Oil Corporation (IOC), Oil India (OIL) and BPCL are buying a 29.9 per cent stake in Russia's Taas-Yuriakh oilfield for $1.28 billion (Rs 8,800 crore). They will also incur capex of $180 million (Rs 1,197.6 crore) on the fields, which have proven reserves of 137 million tonnes. These are already producing 20,000 barrels per day (bpd) and are expected to reach peak output of around 100,000 bpd by 2021. The valuation is comparable to the $2.1 billion Rosneft paid for 65 per cent in the oilfield in 2013, when prices were higher.

In another deal, ONGC Videsh (OVL) is buying an additional 11 per cent stake in the Vankor oilfield for about $920 million (Rs 6,122.6 crore) from Rosneft, increasing its stake to 26 per cent, not very different from the $1.27 billion OVL paid to acquire 15 per cent in the oilfield in 2015. In the same field, IOC, BPCL and Oil India are acquiring 23.9 per cent for about $2 billion (similar valuations). That Vankor, Russia’s second largest oilfield, has low running costs of about $2.22 per barrel of oil equivalent (boe), is in itself a positive.

While OIL, ONGC and BPCL have expanded their exploration and production (E&P) portfolio, the move will give others a footing in the space. That these are already oil producing assets is a positive. While analysts at Ambit believe the acquisition of upstream assets is an ineffective utilisation of cash, given OMCs’ limited knowhow in the E&P space, others point to BPCL's success, a key reason why its stock outperformed PSU peers in longer time-frames.

For OMC’s the bigger positive is the price raise of Rs 3.1 per litre on petrol and Rs 1.9 per litre on diesel taken last week. Market fears that OMCs’ freedom to adjust retail prices, ahead of elections in some states, have thus been put to rest. Gross contribution margins for diesel are now Rs 2.4 per litre and for petrol Rs 2.7 per litre, largely in line with the past six months’ average. Analysts at Ambit say such steep price raises of five per cent are welcome and show that market dynamics will largely prevail on fuel pricing.

First, in the current environment when oil and gas prices are subdued, assets are typically available at reasonable valuations.

Consider this: Indian Oil Corporation (IOC), Oil India (OIL) and BPCL are buying a 29.9 per cent stake in Russia's Taas-Yuriakh oilfield for $1.28 billion (Rs 8,800 crore). They will also incur capex of $180 million (Rs 1,197.6 crore) on the fields, which have proven reserves of 137 million tonnes. These are already producing 20,000 barrels per day (bpd) and are expected to reach peak output of around 100,000 bpd by 2021. The valuation is comparable to the $2.1 billion Rosneft paid for 65 per cent in the oilfield in 2013, when prices were higher.

While OIL, ONGC and BPCL have expanded their exploration and production (E&P) portfolio, the move will give others a footing in the space. That these are already oil producing assets is a positive. While analysts at Ambit believe the acquisition of upstream assets is an ineffective utilisation of cash, given OMCs’ limited knowhow in the E&P space, others point to BPCL's success, a key reason why its stock outperformed PSU peers in longer time-frames.

For OMC’s the bigger positive is the price raise of Rs 3.1 per litre on petrol and Rs 1.9 per litre on diesel taken last week. Market fears that OMCs’ freedom to adjust retail prices, ahead of elections in some states, have thus been put to rest. Gross contribution margins for diesel are now Rs 2.4 per litre and for petrol Rs 2.7 per litre, largely in line with the past six months’ average. Analysts at Ambit say such steep price raises of five per cent are welcome and show that market dynamics will largely prevail on fuel pricing.

Don't miss the most important news and views of the day. Get them on our Telegram channel

First Published: Mar 21 2016 | 9:35 PM IST