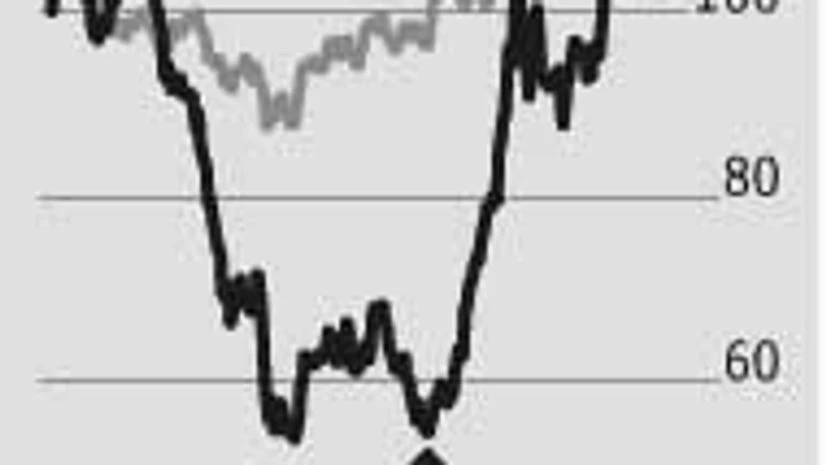

"Punjab National Bank: Rising from the lows")

The Punjab National Bank (PNB) stock is among the top five within the BSE 100 basket to have rebounded in recent months, due to a favourable June quarter.

Just when the Street was readying up for mammoth losses, PNB surprised everyone with net profit of Rs 306 crore in June quarter (Q1). But the key helping factor was its robust forecast on bad loan recoveries and slippages. Recoveries and loan upgrades (NPAs or non-performing assets subsequently upgraded to standard assets) in Q1 stood at Rs 1,840 crore; almost twice the recoveries of December 2015 and March 2016 quarters. Recovery target for FY17 stands at Rs 8,000 crore-10,000 crore and with this gross non-performing asset (NPA) ratio at eight per cent levels. More importantly, investors have been sounded off that they may not see major slippages from accounts put under watch list (Rs 9,860 crore). Watch list comprises of those assets with potential to turn bad. Also, with major accounts in the iron and steel and infrastructure sectors being provided for, the Street is confident that fresh pains may not emerge from these pockets.

In fact, analysts at ICICI Securities believe this strategy, coupled with PNB's focus on recoveries, could keep loan slippages under control. The brokerage recently upgraded its recommendation on PNB to 'buy' from 'hold'. Analysts at Jefferies have a similar view and alert investors to brace up for positive surprises on bad loan formation and recoveries in the coming quarters.

But, dismal capital adequacy remains a worry. Value unlocking from coming listing of its housing finance arm is expected to fetch Rs 2,500 crore for PNB and this could be of some relief. The government is also on track with its bank recapitalisation plan, which analysts at Reliance Securities feel will support PNB's growth in FY17. Valuations are still benign (0.77x FY17 price-to-book value), adding support to investment sentiment.