)

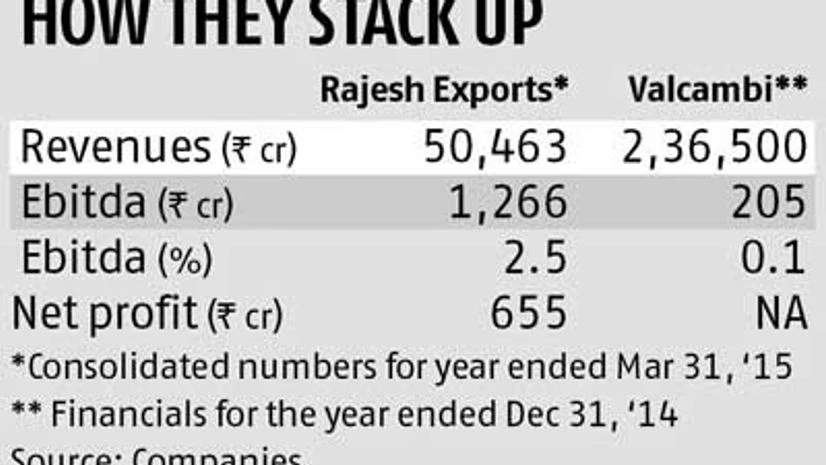

Rajesh Exports (REL) shares made a new high of Rs 556 apiece on Tuesday following its acquisition of Valcambi, the world’s largest precious metals’ refinery, for $400 million or about Rs 2,600 crore. With this acquisition, the jewellery manufacturing and exporting company has taken one step towards backward integration. The acquisition will be positive for the company given that it will help bring down its costs of sourcing gold. The company can now directly source gold from Valcambi that will help reduce the premium it pays while buying gold, says an analyst. The move for Rajesh Exports, which also retails jewellery in the domestic market, should thus lead to better margins. It’s chairman Rajesh Mehta says the acquisition will help lower sourcing costs by 0.1-0.2 per cent, which given the turnover will mean a saving of Rs 50-100 crore annually. Valcambi’s annual revenues are almost four times that of Rajesh Exports, but the latter enjoys much higher earnings before interest, taxes, depreciation, and amortisation margins.

According to analysts, with this acquisition, Rajesh Exports can scale up its margins but the actual gains will be contingent on successful execution by the company management. However, there are other issues that need to be addressed.

“While the acquisition can boost Rajesh Exports’ profits, we will advise investors to wait and watch to get adequate confidence on execution plan of the company,” says a fund manager. He expressed concerns over the company’s corporate governance practices, which some other experts in the market also share.

ALSO READ: Rajesh Exports to foray into gold finance biz

Analysts say it is thus not surprising that the REL stock trades at a visible discount to some of its peers. Mehta, however, denies any such concerns saying the company follows the best practices, which is also reflecting in its share price returns.

Rajesh Exports wants to leverage Valcambi ‘s brand name and business to supply gold to banks and retailers, and earn a 5-7 per cent premium on the gold value by selling gold bars. The company also plans to scale up its domestic retail business, which currently forms less than two per cent of its revenues. However, intense competition from both organised and unorganised jewellery retailers will be a key challenge for the company, which sells under the Shubh brand.

What’s also worrying analysts is the sharp 2.5 times increase in REL’s stock in the past three months, which indicates most positives are adequately priced in.

Arun Kejriwal, founder of Kejriwal Research and Investments Services, says, “Given that REL produced average 900 tonnes in the past three years, the deal will not bring significant gains for the company. The stock trades at 24 times FY15 earnings versus 20 times for PC Jewellers and appears expensive. I advise investors to watch out for any improvement in the company’s results in another couple of quarters before making any investment.”