"Vandana Gombar: Solar to dominate global power map")

What will the electricity sector look like in 2040? What will be the share of renewables? There are projections from the International Energy Agency (World Energy Outlook) and the Energy Information Administration of the US (International Energy Outlook). Bloomberg New Energy Finance (BNEF) published its New Energy Outlook (NEO) 2016 earlier this month. The latter is the most aggressive on renewables build, and the most conservative on the roll-out of new fossil fuel capacity.

BNEF expects $11.4 trillion to be invested in power generation over the next 25 years, till 2040, of which over two-thirds would be in renewables. The projection takes into account intelligence from our project pipeline database, as well as the impact of current policies. In the medium to long term, it bases these projections on the economics of building renewables.

While coal and gas are expected to get even more competitive, NEO 2016 projects a steeper fall in the cost of renewables, and hence an accelerated roll-out. The main headlines of the forecast are:

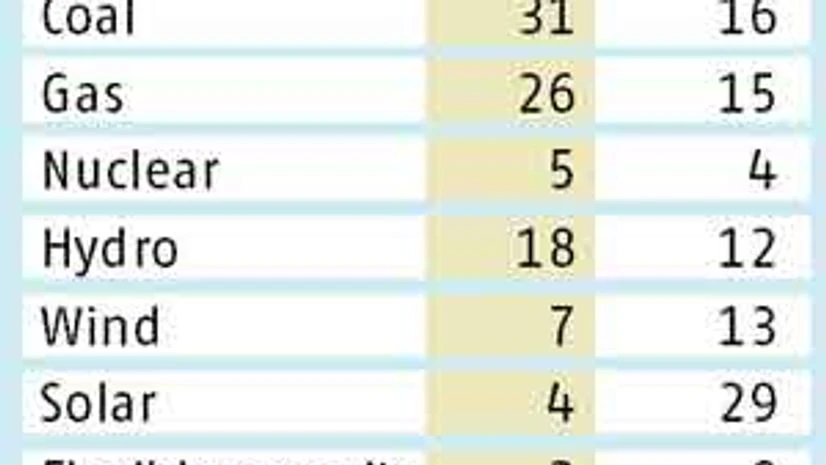

> Solar would have the largest installed capacity by 2040: Power from the sun would account for almost 30 per cent of the global installed capacity. Currently, solar accounts for 4 per cent of the total installed capacity. Wind power would grab a 13 per cent share, against 7 per cent currently. Coal would shrink to 16 per cent of installed capacity, from 31 per cent, while gas would account for 15 per cent (see table).

Solar is already the most competitive source of power in some regions. The most recent bid in Dubai, for an 800MW solar plant, is at a record low of 2.99 US cents per unit. Zambia has managed to secure the cheapest solar power in Africa with a bid of 6.02 US cents through a programme backed by the World Bank. For comparison, the lowest bid in India — which is a much more mature market with over 7GW of solar installed — is at Rs 4.34 per unit, or 6.43 US cents per unit at the current exchange rate.

> Flexible capacity would account for 8 per cent of installations: Flexible capacity, which includes power storage, demand response, virtual power plants, flexible distributed capacity and other potential resources, would rise substantially from the current level of 2 per cent of the overall energy mix. The supply and demand for power need to be matched over the long term (years to months ahead), the short term (days to minutes ahead) and in the immediate moment to control frequency.

Storage is not yet competitive for India per se, as we know, but solar bids are starting to have a layer of storage, and developers are getting into pre-bid arrangements with storage companies. Skypower announced that it would partner with China’s BYD Company for bids of up to 750MW in India. BYD is backed by Warren Buffett’s Berkshire Hathaway.

> Electric vehicles will add significantly to power demand: We forecast that electric vehicles will account for 35 per cent of new global passenger vehicle sales by 2040, from about 1 per cent today. This will be driven by falling battery prices and improved vehicle performance, which would push total cost of ownership below that of internal combustion vehicles on an unsubsidised basis.

China is trying to take the lead in electric vehicles, as it did in the wind and solar sectors. There are Chinese companies vying to be the next Tesla, and the state is backing the industry by supporting the roll-out of charging infrastructure, in addition to providing subsidies for these vehicles.

Storage, solar and electric vehicles may be on course to marry, with Tesla Motors making a $2.86-billion offer to buy SolarCity. Both the companies are backed by Elon Musk, who described the combination as “blindingly obvious”.

Given that India will be one of the top five (or even top three) solar markets in the world, there are some who make a case for seeding a domestic manufacturing industry for batteries and solar panels under the government’s “Make in India” initiative. There does not seem to be an inherent competitive advantage that India can exploit in this sector, nor does it have the deep pockets that China has to create a competitive advantage. Given that there is a higher tariff allowed for domestically made panels since they cost more, such a move may actually come in the way of the “power for all” initiative.

The author is editor, Global Policy, for Bloomberg New Energy Finance; vgombar@bloomberg.net

Disclaimer: These are personal views of the writer. They do not necessarily reflect the opinion of www.business-standard.com or the Business Standard newspaper