)

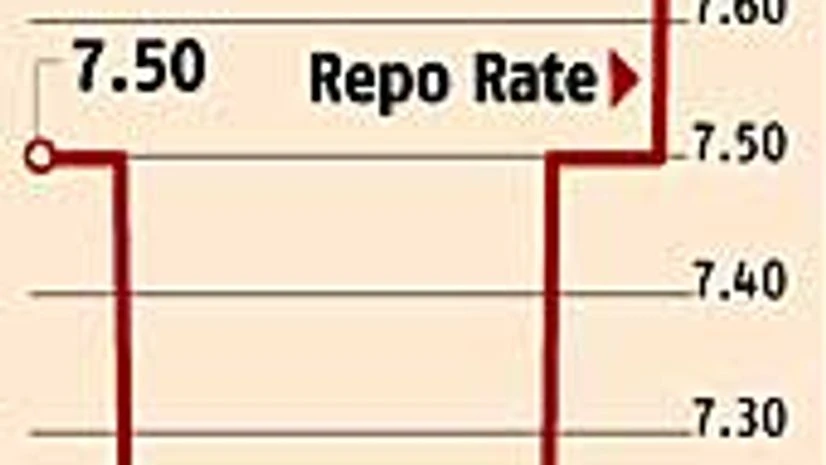

After surmounting the currency crisis, Reserve Bank governor Raghuram Rajan has trained his guns on inflation. By bringing the differential between the marginal standing facility and repo rate to 100 basis points, Rajan has put an end to the back-door tightening route taken by his predecessor D Subbarao. With Tuesday's 25-basis point repo rate hike, RBI has opted to reverse the trend of rate cuts in the first five months of 2013.

Subbarao had cut rates thrice in the year, bringing down the repo to 7.25 per cent. In hindsight, economists question these cuts, with concerns on inflation nowhere over. Kruti Shah, economist at Karvy Stock Broking, says Rajan has taken away the feel-good picture painted by his predecessor while cutting rates earlier this year.

Tuesday's policy statement has put inflation back in the spotlight, as the central bank expects both retail and wholesale inflation to remain elevated through the year. For a change, economists have been in favour of a rate hike, as real effective interest rates have been in the negative zone if one factors in high retail inflation.

According to Nomura's Sonal Varma, given the current high consumer price index inflation, the present repo rate has been persistently below the neutral rate, implying monetary conditions have been too loose. So, the recent repo rate hikes are intended to align interest rates to "real" domestic inflationary conditions.

Other economists say with savings falling sharply, the policy statement contains little to address that. Also, the repo hikes will do little to tame inflation driven by government spending. The focus on cheaper consumer loans is in contrast to RBI's suggestion to banks on shoring up deposits.

What the policy fails to provide is guidance. While the policy statement expects inflation to stay elevated, it doesn't spell out any level. Dhananjay Sinha of Emkay Global says: "The statement fails to provide forward-looking guidance and is a dilution in terms of content and foresight. RBI has refrained from providing categorical projections like wholesale price index inflation, projections on monetary aggregates such as money supply, bank deposit and credit growth."

The implicit understanding is that the central bank's actions will be driven by data points, as and when these emerge.