)

Consumers have already faced a railway price rise, petrol and diesel increase and rising inflationary pressure. Now, all eyes are on Finance Minister Arun Jaitley to provide some semblance of the much-touted ache din.

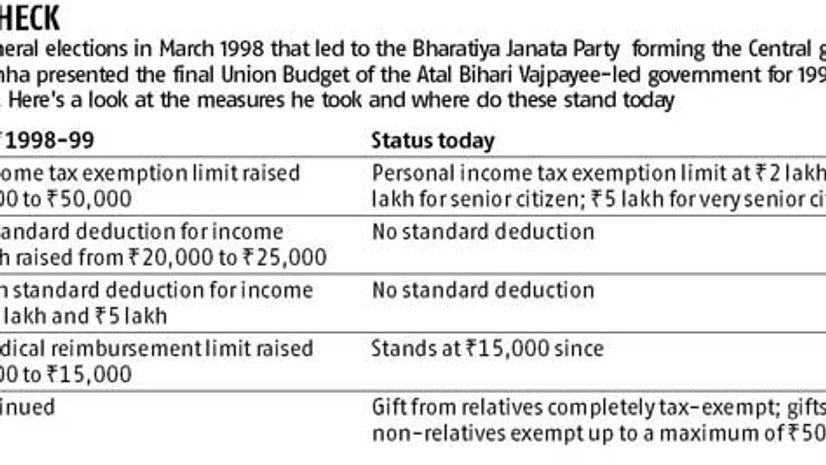

But going by the record and the government finances, things might not change dramatically. The Bharatiya Janata Party-led National Democratic Alliance came to power for the first time in 1998 (for 1998-99). Finance Minister Yashwant Sinha, in his first budget, had made some minor changes in direct taxes - the exemption limit was increased from Rs 40,000 to 50,000. Standard deduction or basic exemption limit for incomes of Rs 1 lakh was raised from Rs 20,000 to Rs 25,000.

His biggest gift to income-tax assessees was increase in the medical reimbursement from Rs 10,000 to Rs 15,000, a number that has remained unchanged for a decade and a half (see table). Rajesh Srinivasan, partner at Deloitte, Haskins and Sells LLP says that Jaitley could start by revising this limit first.

There are many other expectations, ones Jaitley may or may not be able to deliver on. Like, increasing the basic income tax exemption and Section 80C limit.

Reports say Jaitley is more likely to disappoint the taxpayers on these two fronts. Experts are on the same page. Chartered accountant Parizad Sirwalla says on the personal taxation front there are very little that the finance minister might do this time. "Upwards revision in slab rates may not come about so soon," she says.

Reason: The economic condition of the country is not very good. The monsoon has been below expectation. India is fearing an oil crisis due to the Iraq troubles. And the new government did not get enough time to prepare for this Budget.

Taxpayers were expecting the income tax exemption limit would be raised to Rs 5 lakh and/or the deduction limit be raised to Rs 2 lakh. The current basic exemption limit is Rs 2 lakh, Rs 2.5 lakh for senior citizen and Rs 5 lakh for very senior citizens (80 years and more). Section 80C allows deduction of up to Rs 1 lakh, set in 2006.

Suresh Surana, founder of tax consultancy firm RSM Astute Consulting says expectations of raising the basic exemption limit to Rs 5 lakh may be a bit far fetched due to the high fiscal deficit and slow economic growth. At best, the government may look to revise the limit upwards to Rs 2.50 lakh and the investment limit to Rs 2 lakh.

Given income tax has been a pain point for the aam aadmi for ages, Jaitley is positively expected to offer some relief to taxpayers.

Here's a list of the expectation from the Union Budget 2014-15:

Reintroduce 80CCF bonds

Union Budget 2011-12 had introduced Section 80CCF under which annual investments of up to Rs 20,000 in long-term infrastructure bonds were exempt from tax. However, this was not extended in Finance Bill 2012-13.

Sirwalla feels as the emphasis of the new government is on infrastructure, reintroducing 80CCF infrastructure bonds could be a good idea. It would help taxpayers get additional deductions. Some others feel the Rs 20,000 limit is too low and could be revised to Rs 50,000.

Relook at LTA limit

Experts feels Leave Travel Allowance (LTA) should incorporate more than it does. "Given the spending and lifestyle changes of individuals, LTA exemption should be extended to overseas travel and should also cover stay and food expenses," says Kuldip Kumar, executive director, tax & regulatory services - personal tax at PwC.

At present, the salaried can claim the travel expense of his and family members (dependent spouse, two children, brothers, sisters and parents) within the country. Expenses on stay, sightseeing and food aren't included. The allowance can be claimed twice in a block of four calendar years. The block being considered presently is January 1, 2014 to December 31, 2017.

Hike limit for loan interest repayment

Amarpal Singh Chadha, tax partner at EY, feels it's time the exemption limit for interest repayment towards a housing loan for self-occupied house properties be revised upwards, given the rate at which property prices have moved up. According to National Housing Bank's residential index (residex), property prices have run up by an average of 20 per cent in Mumbai between January-March 2012 and January-March 2014. In individual areas, the rise has been steeper.

The deduction for interest repayment of up to Rs 1.50 lakh might not work for metro cities, where home cost is way higher than the Rs 15-18 lakh loan amounts (which would provide a Rs 1.50-lakh benefit). For a home loan of Rs 50 lakh, the equated monthly instalment (EMI) would be roughly Rs 50,000. Of that, at least 80 per cent goes towards servicing the interest portion, which comes to Rs 40,000 or Rs 4.80 lakh annually. One gets tax benefit on only Rs 1.50 lakh of that, unless it is a second property. You get unlimited tax benefit for repaying interest on a second home loan.

Introduce higher super rich slab, remove surcharge

At present, the super -rich or those with annual income of Rs 1 crore or more are levied a surcharge of 10 per cent. Surcharge is levied on the slab rate, in this case, 30 per cent. This works out to an additional three per cent tax for those earning Rs 1 crore or more.

Srinivasan feels it might be a better idea to introduce another slab rate for the super-rich and remove the surcharge. Experts feel the tax slab rates for such individuals could be 35 per cent.

Introduce standard deduction

Srinivasan says reintroduce standard deductions for inflationary adjustment. "Club all allowances and look at standard deduction linked to inflation. This may impact the direct tax collections but will help increase taxpayers' spending activity and, thus, help the government increase indirect tax collection," he explains.

If not that, at least consolidate the smaller deductions, says Surana. For instance, Section 80CCG which allows deductions for investment up to Rs 25,000 in the Rajiv Gandhi Equity Saving Scheme, Section 87A under which taxpayers with income of Rs 2 lakh to Rs 5 lakh get a tax credit of Rs 2,000 and Section 10(32) where income of minor children are exempt up to Rs 1,500.

"An investment limit of Rs 25,000 which translates to a maximum benefit of Rs 7,500 is way too small to claim for separately. Similarly, we can do away with the tax credit bit as the amount involved is too small. Section 10(32) will translate into a benefit of Rs 450 for those in the highest tax bracket. It's better to consolidate these under one section like 80C," he says.

Introduce joint return filing

Finally, Srinivasan suggests introducing joint filing of tax returns by spouses. This would help save on some taxes. This is common in the US, where legally married couples can choose to file joint returns. This also provides more tax benefits than filing separately.

Or, introduce tax deductions linked to the family size. In the US, The Earned Income Tax Credit (EITC) varies based on income and family size. For instance, those who qualify for EITC for tax year 2013, can get a credit from: $2 to $487 with no qualifying children; $9 to $3,250 with one qualifying child; $10 to $5,372 with two qualifying children; $11 to $6,044 with three or more qualifying children.