"Mis-selling: You are on your own")

Atypical sales pitch: Sir, we are selling an open-end mutual fund (MF) which will give tax-free returns. The scheme returned 15 per cent last year.

Ideally, your answer should be: The only MF scheme that can give me tax-free returns is an Equity-Linked Savings Scheme (ELSS) but it has a lock-in period of three years.

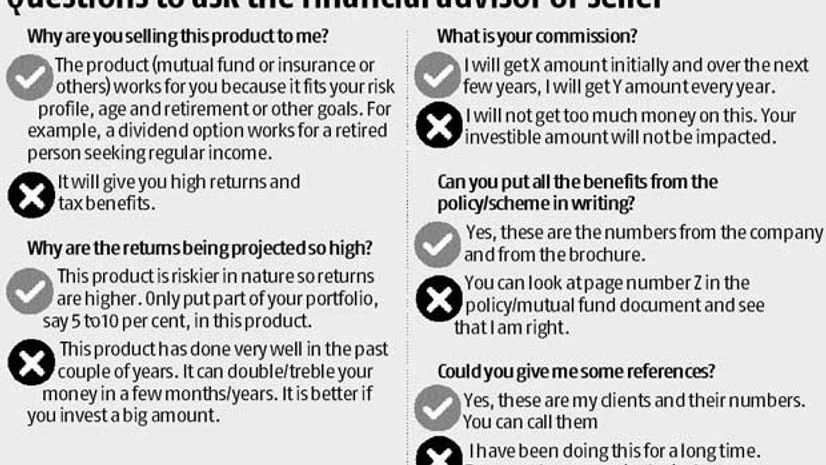

Most of us don't ask these questions and get hustled into buying something we don't know much about. Worse, sometimes, investors are sold insurance schemes as MF schemes.

Obviously, regulators are worried. In the foreword to the recently issued annual report of the Reserve Bank of India (RBI), the governor promised to focus on mis-selling of insurance by banks. The Insurance Regulatory and Development Authority of India (Irdai) is also planning to have different commission structures for agents and the bancassurance channel. In effect, the incentive for bank staff to mis-sell will come down. While the regulators continue to grapple with the situation, the onus still rests on the buyer to protect himself against mis-selling.

Mis-selling by banks

Banks have emerged as the big culprits in mis-selling. Sales persons from banks, under tremendous pressure to meet targets, mis-sell insurance products and MFs to many a lay investor.

They have got away with it so far because India has multiple regulators. Banks' selling of products like insurance and MFs falls in what is referred to as 'regulatory cracks' or 'regulatory no-man's land'. While banks are regulated by RBI, the third-party products sold by them are regulated by the Securities and Exchange Board of India (MFs) and Irdai (insurance). According to Manoj Nagpal, chief executive officer (CEO), Outlook Asia Capital, "Mis-selling by banks will stop only once RBI initiates punitive action against senior-level management, on whose direction the junior personnel do the mis-selling."

How is it done?

In the financial sector, this can be done in various ways. In many cases, it is the advice given that is wrong, and, hence, difficult to prove.

Insurance: While selling a traditional insurance product (like endowment), the seller could promise guaranteed returns of eight per cent annually plus bonuses. "Most buyers today are aware that Ulips (unit-linked insurance plans) don't offer guaranteed returns. But, many still get fooled into believing that traditional products do so," says Arvind Laddha, CEO, Vantage Insurance Brokers. Ideally, they should be showing two numbers: Returns at four per cent and eight per cent, as a mandate by Irdai. However, many choose to show the higher number. Sales of a high-value term cover to a senior citizen who doesn't any longer require protection against the risk of dying early is another common trend.

Health insurance: Say, a Rs 15-lakh product is sold to a 20-something couple. The question: Do they really need it? The mis-selling here also lies in the fact that the couple could as well buy a Rs 5-lakh base cover and a Rs 10-lakh top-up, which would be cheaper.

Sometimes, in the case of high-value health covers, there could be a promise of both out-patient and hospitalisation expenses being covered, when only the latter is covered. The seller could also promise that you would be covered globally whereas you are covered only within the country.

Tax-saver funds are also sold to the extent of Rs 5-10 lakh for their higher commissions, when the tax deduction limit is only Rs 1.5 lakh. "Avoid buying ELSS beyond the tax benefit. Meet your investment needs through open-ended diversified equity funds," says Srikanth Meenakshi, founder-director, Fundsindia.com. He also warns against buying closed-end funds. "Don't get into a fund which doesn't offer you the flexibility to exit if it underperforms," he adds.

Home loan: When a customer takes a home loan, he should ideally be sold a mortgage cover or a term cover, to insure against the massive liability he has taken on. In fact, RBI does not allow bundling of products. So, in ideal circumstances, the bank or financial institution providing the home loan should not offer any products. The common situation is that he is mis-sold an insurance-cum-investment product, on which the premium, and hence commission, is higher. Sometimes, purchase of the insurance is made a pre-condition for sanctioning of the loan.

Regulatory shift required

Today, the buyer finds it very difficult to prove mis-selling once he has signed the application form. And most sign them without reading them. In India, the regulatory regime is that of caveat emptor or buyer-beware. Globally, the regulatory regime is shifting towards caveat venditor or seller-beware. Under this regime, if there is a complaint of mis-selling, the onus is on the seller to prove innocence.

Till this shift happens, one recommendation made by the Sumit Bose Committee needs to be implemented at the earliest. "With each financial product, there should be a single sheet on which all important disclosures about the product should be made in large, clear font. Here, it should be stated why the product is suitable for the customer-based on his age, income and risk profile. And, that sheet should be signed by the seller," says Prithvi Haldea, founder-chairman, PRIME Database and a member of the committee.