"graph")

For the past four-five years, the income tax (I-T) department has been consistently tightening its noose around realty transactions. From making registration of rental agreements with PAN details of both the tenant and owner mandatory to the latest — deduction of TDS (tax deducted at source) on monthly rental of Rs 50,000 and above — rules have been tightened significantly to ensure black money isn’t generated from this sector.

The Central Board of Direct Taxes’ (CBDT’s) latest salvo targets people who claim significant amounts as house rent allowance (HRA), sometimes with the help of false documents. From June onwards, those who pay monthly rental of Rs 50,000 need to deduct 5 per cent TDS and deposit it with the I-T department. This TDS trail will serve as proof for people claiming high HRA. The provision was introduced in the Finance Bill, 2017. “The idea behind the provision is to make sure taxpayers don’t claim fake HRA exemption and also to trace those who don’t disclose their rental income. When a trail is created, it will be possible to detect such individuals in the system,'' said Kuldip Kumar, partner and leader, personal tax, PwC India.

Interestingly, the government has also made the provision that if multiple tenants stay at the same place and pay total rent of Rs 50,000 and above per month, they need not deduct TDS. But, all tenants’ names should be in the registered agreement with the owner. On the other hand, if the entire rent is paid by a single tenant and the others are merely paying that person, then TDS is applicable. Clearly, CBDT has given relief to people staying together, especially in big cities and paying high rent to stay near their office or for any other reasons.

The procedure is similar to deducting TDS while purchasing property, where the buyer has to deduct TDS of 1 per cent. Under Section 194-IB, tenants have to deduct TDS at the rate of 5 per cent and deposit it with the government within a month’s time. “If the tenant does not deduct the TDS or fails to deposit the tax with the government, both tenant as well as landlord will have to pay penalty and interest,” said Naveen Wadhwa, general manager, Taxmann.com. The penalty for not deducting TDS and not depositing the tax with the government is 1 per cent and 1.5 per cent, respectively, per month.

Things have been simplified further by allowing TDS to be paid without any requirement of TAN (Tax Deduction and Collection Account Number). By simply using the tenant and landlord’s PAN, the tax can be paid.

The tenant has to file form 26QC and deposit the money with the government. This is to be done online through the I-T department’s website, using the tenant and landlord’s PANs. If the landlord’s PAN is not available, then tax has to be deducted at 20 per cent, instead of 5 per cent. After filing form 26QC, the tenant has to generate Form 16C and issue it to the landlord within 15 days. Form 16C is the new form for taxes deducted on rental, like Form 16 for salaried individuals, Form 16A for interest payment and Form 16B for purchase of immovable property.

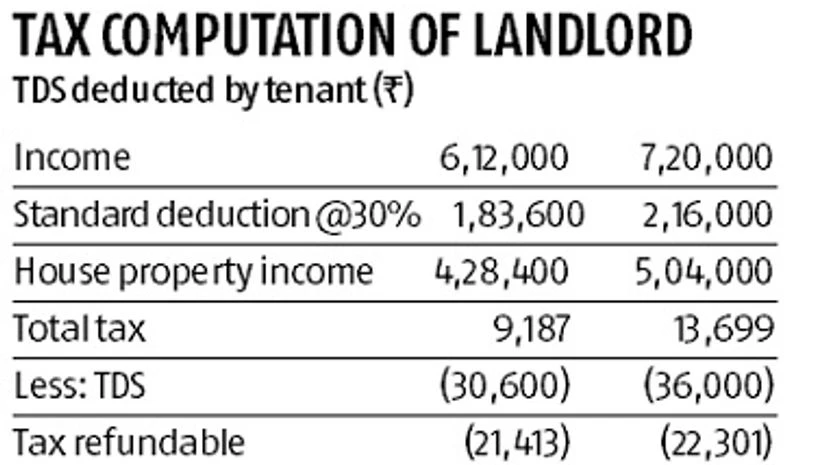

“Since the tenant is deducting TDS, the landlord will have to disclose rental income. If the TDS is not deduced, the landlord cannot take credit and he will have to pay tax. And if the TDS is deducted, the landlord can take credit and file for refund, if any,” said Archit Gupta, founder and CEO, Cleartax.com.