)

A month or so after the oath-taking, the euphoria has somewhat abated. Expectations about the Budget are also gradually coming closer to the rational. The ratings for the new government are still excellent. But there have been missteps with the rail fare hike. The delayed gas-price hike has disheartened traders hoping for big-bang reforms. Developments on the monsoon front have been inimical with heavily deficient June rainfall.

There are also storm clouds on the external front. Iraq continues to be a battlefield and crude prices will fluctuate according to the fortunes of that war. The US has revised its Q1 (January-March 2014) gross domestic product (GDP) numbers down, yet again. That could mean paring down global growth projections.

The hike in railway fares was forced, given the deteriorating finances of the transport behemoth. But the process of raising fares was mishandled. The government raised suburban fares in one fell swoop. This was more than its ally, the Shiv Sena, found acceptable. A smaller hike in suburban fares might actually have worked better.

International Brent crude prices jumped to 10-month highs of $115-plus before there was a little pullback to $113. Iraq's major oil-producing centres in the South have not been hit so far. But the largest Iraqi refinery is in the conflict zone. There is no telling if the Islamic State in Iraq and Syria (ISIS) can be contained to its current area of control, let alone pushed back. Nor is there a timeline for resolution of this conflict.

Share prices in energy-related stocks have fluctuated violently since Iraq blew up. The rupee has also come under some pressure. India imports 80 per cent of her crude and there is a straightforward relationship between crude imports and the current account. Quite apart from the potential economic impact of an oil shock, there are also many Indians in the conflict zone. Some 40-odd have been kidnapped and getting them out safely will be an acid test of India's diplomatic skills and soft power.

The domestic oil subsidy was a massive Rs 1,40,000 crore in 2013-14. Retail pricing controls leads to under-recoveries for public sector undertaking (PSU) retailers such as BPCL, HPCL and IOC. The Government of India bears about half of this subsidy directly via oil-bonds. PSUs such as ONGC, GAIL and OIL pick up the rest of the tab. This hurts minority shareholders in PSU energy stocks, as well as the government, of course.

The decision to delay a hike in domestic gas prices for three months was not unexpected. It has, however, disappointed those who were gambling on a quick reboot of energy subsidy policies. Gas is very sensitive. There is the Reliance KG-D6 imbroglio. A gas-price hike may also lead to enhanced subsidies for individual homes and for public transport, as well as for bulk-consumers like power and fertiliser. If price hikes are passed through, it would trigger inflation and resentment.

But the dependence on gas imports will increase over the medium term. Substantial infrastructure - terminals, regasification facilities, pipelines and so on - is being developed in anticipation. It, therefore, makes sense for domestic gas prices to be linked to international rates since the subsidies will balloon otherwise.

Long-term contract rates in gas vary widely from spot cargo rates. Transport costs are huge. Prices may fall dramatically if the US allows shale gas exports. GAIL is seeking US tie-ups in those hopes. If the Ukraine crisis continues, prices could rise since Russia supplies much of western Europe's gas via Ukraine. There is even a chance that India will be able to negotiate good rates for Russian gas, by fishing in troubled waters.

Meanwhile, the US has revised its Q1-GDP numbers down. The American economy contracted by 2.9 per cent, which was thrice the earlier estimate of minus one per cent. Sentiment remains strong, with Wall Street indices hitting new highs. The US Fed appears determined to carry on tapering.

Apart from external issues of this nature, the government will have to cope with the twin threats of high inflation and drought. Monsoon failure looks pretty much on the cards. How the government handles food inflation could determine what the Reserve Bank of India does to interest rates.

A minimum export price on potatoes could deter exports. Ideally, of course, the Centre should try and persuade states to rationalise respective agriculture produce market committees, which offer so much scope for price distortion and manipulation. It is anyone's guess if it will try to do this.

It may have been a good thing that the government was forced to roll back rail fares. It means that the Budget is more likely to pay heed to what measures are politically acceptable, while still attempting to introduce some degree of reform.

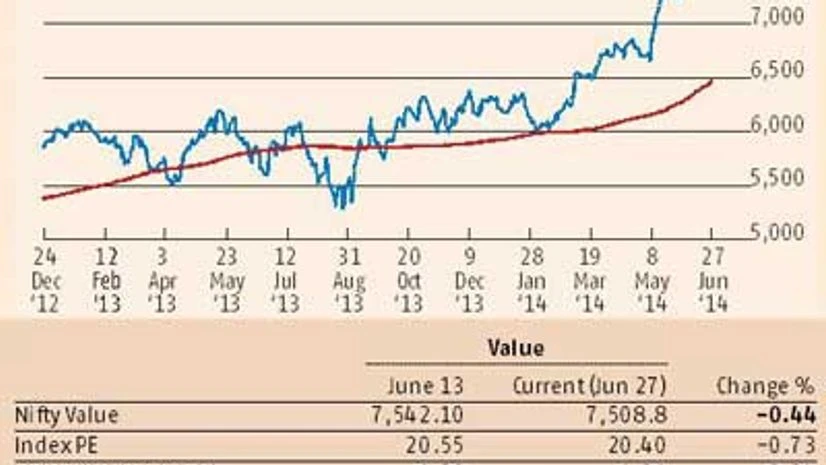

The market has seen some correction and consolidation pre-Budget. It is, therefore, less likely to absolutely crash if the Budget doesn't offer miracles. The short-term trend was negative through the last fortnight. There was net institutional selling. Option chains suggest that market players would be braced for a swing of 500 points in either direction, to Nifty 7,000 or 8,000, once the Budget comes through.

Politics is often said to be the art of the possible. Many things would be economically desirable but again, many of them would not be politically feasible. Arun Jaitley will have to make that judgement call on July 10.