"Rupee, Indian rupee")

By Andy Mukherjee

A shortage of deposits is starting to unnerve India’s bankers and policymakers. The lenders’ worry is more understandable than the authorities’.

Taking a leaf from a two-decade-old Chinese playbook, the central bank is reining in money growth to tame inflation. In the process, though, it’s putting up a new hurdle in the way of credit and investment. Separately, the government is making the deposit crunch worse by taxing savers aggressively, but keeping the proceeds away from the financial system. Bankers are compounding the problem by not paying enough to savers.

Yet it’s the lenders’ behaviour being put under the scanner. The finance ministry wants depository institutions to undertake special drives to mobilise household savings, while the Reserve Bank of India has warned them that they’re potentially skirting with “structural liquidity issues.” One of them seems to be technology. The RBI wants banks to assume that any customer account connected to a smartphone is prone to faster erosion of deposits.

From next year, banks in India will have to hold more safe assets like cash and government securities to meet the risk of runoff from internet-enabled accounts. While this could slow systemwide credit, some individual lenders will have to do more to get out of their liquidity squeeze. HDFC Bank Ltd., the largest non-state bank, is planning to sell Rs 10,000 crore ($1.2 billion) of its advances to lower its loans-to-deposit ratio, which has exceeded 100 per cent for four straight quarters, according to Bloomberg data.

More than technology, the RBI is worried about greed. For a little over two years, credit has grown faster than deposits. Retail interest in the stock market has exploded in this period. Households that “traditionally leaned on banks for parking or investing their savings are increasingly turning to capital markets and other financial intermediaries,” RBI Governor Shaktikanta Das said in July.

That explanation doesn’t wash. After all, if the asset buyer’s bank balance is debited to pay for securities, the seller’s account is credited. The pie may get redistributed among lenders, and its composition may change. Still, money won’t leave the system, except at ATMs, and the use of cash in transactions is slowing.

More From This Section

"RBI DG Swaminathan Janakiraman")

"Sanjiv Bajaj, president, Confederation of Indian Industry")

"SBI, State Bank Of India")

"GST council meeting")

"Indian rupee, Indian bonds market")

Loans create their own deposits. A new mortgage will eventually show up as a credit entry in the property seller’s account. Sure, loans for foreign education — or buy-now-pay-later credit used to buy imported goods — will leak from the local banking system. But that won’t cause a persistent deposit shortfall. A bigger drain is more likely taking place via taxes, which are sitting in the government’s account with the central bank. That is why state-run lenders are asking New Delhi to park its cash balances with them, instead of the monetary authority.

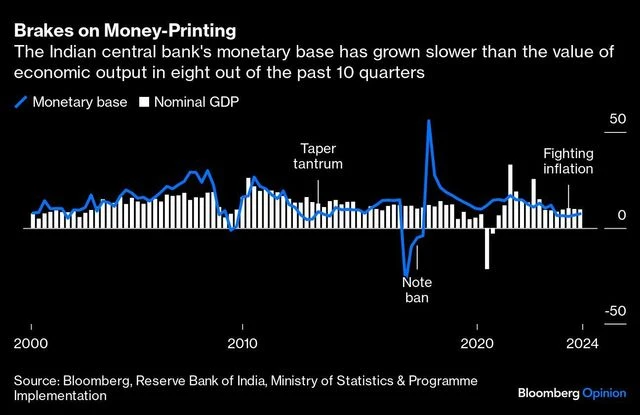

Where the RBI may have played a role in the deposit shortage is in slowing down its printing presses. The sum total of its liabilities — currency held by the public, and reserves that banks keep in their current accounts with the monetary authority — grew 2.3 percentage points slower than the 9.7 per cent expansion in nominal gross domestic product in the June quarter. Last month, the pace of money creation crashed to under 4 per cent.

This is odd. The central bank’s monetary base, also called high-powered money because it fuels credit, tends to run ahead of GDP growth. (The two big exceptions in recent years were during the 2013 taper tantrum and in the aftermath of the sudden 2016 ban on 86 per cent of the currency.)

"chart")

In China, a squeeze on the monetary base used to be a feature of economic management, rather than a bug. The investment boom after Beijing’s 2001 accession to the World Trade Organization could have been exhausting, turning the current account, which represents the excess of domestic savings over local investment, into deficit. Yet China kept racking up higher surpluses.

In a 2007 study, Michael Mussa, a former chief economist at the International Monetary Fund, said the clue to the puzzle lay in the central bank’s balance sheet.

Central banks in developed countries with floating exchange rates buy government securities to print new money. Since having too much of it around is inflationary, interest rates have to rise to cool demand. But China wanted to run its economy red-hot, with an undervalued currency giving it an edge in export markets. So instead of buying bonds, the People’s Bank of China scooped up incoming dollars. And since buying dollars from banks left them with more yuan, the PBOC then mopped up some of that liquidity.

By keeping a tight rein on the monetary base, especially between 2004 and 2006, the PBOC denied households the purchasing power that ought to have resulted from rapid economic growth, forcing them to save more at low, state-controlled deposit interest rates. By engineering a rise in national thrift, China managed to self-finance its growing hunger for investments.

Could India be pursuing a similar approach? It’s no secret that Prime Minister Narendra Modi is aiming to put the economy on an investment-led path of growth with Chinese characteristics. Private final consumption expenditure nowadays accounts for 60 per cent of India’s GDP. That number used to be almost 80 per cent half a century ago. The investment rate, however, is still at about 31 per cent of output.

Never mind the 45 per cent rate at which capital formation in China peaked in 2013. Can Modi raise the investment-to-GDP ratio to 36 per cent, the high achieved by India before the Global Financial Crisis of 2008-09? Even the recovery from that shock ended abruptly in 2013 as domestic savings ran out, and foreigners balked from financing the country’s high current-account deficits.

Since then, the current account has been well behaved, and unlike a decade ago, banks are well capitalised. This time around, the vulnerability may be building elsewhere. It’s the lenders’ deposit shortage that could put a speed limit on credit-fueled investment — unless authorities come up with some ingenious ways to keep banks lubricated while putting a lid on money creation.

Disclaimer: This is a Bloomberg Opinion piece, and these are the personal opinions of the writer. They do not reflect the views of www.business-standard.com or the Business Standard newspaper

"housing, housing finance")

"RBI, Reserve Bank of India")

"Street vendors, Street Hawkers")

"RBI, Reserve Bank of India")