"Vehicle scrappage policy")

Countries across the world have set ambitious targets to achieve net-zero carbon emissions. In their efforts to reach these goals, the European Union (EU) has implemented a carbon tax on imported goods with high-energy intensity, under the banner of the Carbon Border Adjustment Mechanism (CBAM). CBAM represents a unique non-tariff measure (NTM) that can be quantified much like traditional tariffs. It is expected that other countries will soon follow the suit, as is often the case in international trade, where there are typically two possible Nash equilibriums: either no nation enforces trade measures, or every nation adopts them.

One sector poised for significant impact is the Indian steel industry. Currently, the Indian iron and steel sector stands as the largest consumer of energy within the manufacturing sector. Carbon dioxide (CO2) emissions from Indian steel production range from 2.5 to 2.85 tonnes per tonne of crude steel, in contrast to the global average carbon intensity of 1.4 tonnes per tonne of steel, according to the International Energy Agency (IEA). This disparity can be primarily attributed to differences in production techniques. According to the Ministry of Steel's annual report 2022-23, approximately 70-75 per cent of steel is produced either through the Blast Furnace – Basic Oxygen Furnace (BF-BoF) route or Direct Reduced Iron (DRI) based route with coking coal serving as the primary reductant. In contrast, other major steel-producing nations like the European Union, Japan, and the USA commonly employ the Electric Arc Furnace (EAF) route for steel production. The choice of production technique in different regions can be influenced by various factors, but one of the primary factors is the availability of low-cost raw materials, which primarily depends on factor endowment. In the case of India, where iron ore, a key raw material to produce steel, is readily available at an affordable price, most companies prefer to rely on the BF or coal-based DRI route to produce steel.

With the current shift towards internalizing negative externality (i.e. taxing carbon emissions associated with steel production), Indian companies will need to explore greener alternatives for steel manufacturing. One approach is to use green hydrogen instead of coke or coking coal in the Blast Furnace (BF) route. However, the production cost of green hydrogen in India stands at approximately $4 to $5 per kilogram, significantly higher than the cost of coke or coking coal, which is around $0.1 to $0.2 per kilogram, rendering it economically unviable. Another potential solution is the implementation of Carbon Capture, Utilisation, and Storage (CCUS) technology. Nevertheless, there are numerous challenges associated with the widespread adoption of this technology.

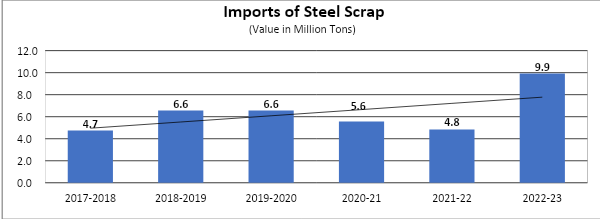

One effective strategy to reduce carbon emissions is to adopt the Electric Arc Furnace (EAF) route, similar to other countries. In the EU, steel produced using the EAF method emits just 0.33 tonnes of CO2 per tonne of crude steel. According to the Joint Plant Committee of the Ministry of Steel, the electric arc furnace method already accounts for 25 per cent of crude steel production in India, suggesting that it could be a viable solution to this challenge. The primary raw material for producing steel using the Electric Arc Furnace (EAF) method is steel scrap. The EU largely produces this scrap domestically. However, in India, a significant challenge arises due to the limited availability of steel scrap. This scarcity has led to the import of approximately 10 million tonnes in the financial year 2023. It is important to note that relying on imports in the long term may not be a sustainable option, especially as more countries are imposing export restrictions on steel scrap.

Source: Joint Plant Committee

Boosting domestic production of steel scrap can be achieved by increasing the production of vehicle scrap. The successful implementation of the new Vehicle Scrappage Policy (VSP), 2022, has the potential to significantly enhance the availability of steel scrap within the country. This, in turn, could lead to a reduction in the prices of scrap steel, thereby enhancing competitiveness in the market. Earlier, the definition of End of Life Vehicles (ELVs) in India remained unclear and open to interpretation, which has led to a lack of regulatory guidance in the industry. However, starting from April 1, 2023, mandatory fitness tests for commercial vehicles are proposed to be conducted exclusively through Automatic Testing Stations (ATS). In contrast, passenger vehicles are slated to have mandatory fitness tests at ATS commencing on June 1, 2024. Commercial vehicles will be required to undergo annual fitness tests after 8 years from their initial registration, whereas passenger vehicles must renew their fitness tests 15 years after their registration, valid for a period of 5 years. Any vehicle that fails its fitness test will be designated as an 'end of life vehicle' (ELV).

ELVs, which are critical sources of recyclable materials, are predominantly processed by the informal sector, making it difficult to obtain official figures on steel scrap production in the country. Although the informal sector plays a vital role in recycling, it operates with limited resources, relying primarily on low technology and labour-intensive methods. To encourage the scrapping of old vehicles by the formal sector and promote the adoption of newer, more environmentally friendly models, several incentives and disincentives have been introduced. These incentives encompass registration fee waivers for new vehicle purchases, potential state refunds of 15-25 per cent on motor vehicle taxes, up to a 5 per cent discount from auto manufacturers when buying new vehicles, and a scrap value payout to the vehicle owner, equivalent to 4-6 per cent of the new vehicle's ex-showroom price. Disincentives include increased fitness test and fitness certificate fees for commercial vehicles older than 15 years and raised re-registration, fitness test, and fitness certificate fees for passenger vehicles exceeding the 15-year mark.

According to a report by the Centre for Science and Environment (CSE), it is estimated that approximately 2.25 million vehicles, including two-wheelers and commercial vehicles, will become obsolete by the year 2025 (as shown in the table below). This translates to a significant 9 million tonnes of steel, approximating the annual imports of steel scrap in 2022, and contributing to substantial import substitution. Furthermore, the number of vehicles reaching the end of their operational life is expected to continue growing in the future.

Table: Expected Steel Scrap Generation from Automobile Sector

Source: Ficci 2018, 'Accelerating India’s Circular Economy Shift: A half a trillion USD opportunity'

As per the National Steel Policy (2017), it is envisaged that production and consumption of finished steel are expected to reach 230 million metric tonnes and 206 million metric tonnes respectively by 2030. Out of the total finished steel production of 230 million metric tonnes, it is anticipated that 35-40 per cent will come from scrap-based steel production. This means that the demand for steel scrap will rise significantly, increasing from the current level of approximately 30 million tonnes to over 70 million tonnes by the year 2030.

The effective implementation of VSP will lead to the killing of two birds with one stone. First, it will help India to reduce carbon emission levels leading to alignment with the growing environmental regulations such as CBAM. Second, it will help to achieve the target of the National Steel Policy (2017). The vehicle scrappage policy holds immense potential for enhancing the international competitiveness of the Indian steel industry.

(Aishwary Kant Gupta is consultant at Ministry of Commerce and Industry, New Delhi; Zaki Hussain is consultant at Ministry of Commerce and Industry, New Delhi)

Disclaimer: These are personal views of the writers. They do not necessarily reflect the opinion of www.business-standard.com or the Business Standard newspaper

Disclaimer: These are personal views of the writers. They do not necessarily reflect the opinion of www.business-standard.com or the Business Standard newspaper