"US job")

By Vince Golle and Craig Stirling

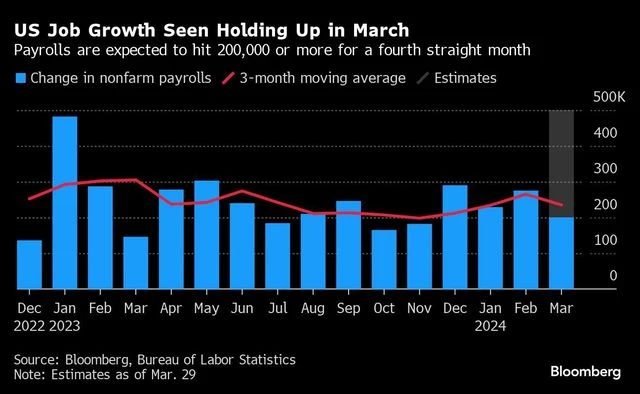

Healthy US employment gains continued in March while wage growth moderated, indicating the nation’s labor market is poised to keep stoking the economy with limited risk of an inflation resurgence.

Payrolls in the world’s largest economy are seen increasing by at least 200,000 for a fourth straight month, according to a Bloomberg survey of economists. Average hourly earnings are projected to climb 4.1 per cent from the same month last year, the smallest annual advance since mid-2021.

"chart")

Resilient hiring is keeping demand and the economy moving forward at the same time inflation is slowing, albeit unevenly. It’s also allowing Federal Reserve policymakers to hold off reducing interest rates as they await further declines in price pressures.

Resilient hiring is keeping demand and the economy moving forward at the same time inflation is slowing, albeit unevenly. It’s also allowing Federal Reserve policymakers to hold off reducing interest rates as they await further declines in price pressures.

Fed Chair Jerome Powell, on Wednesday, headlines a large cast of Fed policymakers who are due to speak this week. Among others appearing are John Williams, Adriana Kugler, Mary Daly, Austan Goolsbee, Lorie Logan and Thomas Barkin.

An increase in labor supply is helping to limit wage pressures that otherwise would risk filtering through to a sustained pickup in inflation.

Friday’s payrolls report is also forecast to show the unemployment rate inched down to 3.8 per cent, just below a two-year high hit in February, suggesting the job market is losing a little momentum.

What Bloomberg Economics Says:

More From This Section

“The two major surveys used to create the jobs report appear to capture different aspects of the US economy. Spending on services by those benefiting from asset price appreciation — mostly baby boomers — has supported employment in leisure and hospitality and health care.

At the same time, reduced demand from the less well-off part of the population has translated to slowing business sales, and reduced hiring or increased layoffs in other sectors. We expect that dichotomy to once again show up in the March report, sending mixed messages to policymakers.” — Anna Wong, Stuart Paul, Eliza Winger and Estelle Ou, economists.

February job openings data on Tuesday will offer a glimpse into labor demand. While economists project a decline, vacancies remain above their pre-pandemic level.

Other reports in the coming week include a pair of purchasing managers surveys from manufacturers and service providers.

Turning north, surveys from the Bank of Canada will offer insights into inflation expectations ahead of its April 10 rate decision. Canada’s jobs data will be released concurrently with the US numbers, and trade data will also be published.

"chart")

Elsewhere, Chinese purchasing-manager surveys are scheduled and a raft of key inflation numbers are due from the euro zone to Turkey to Colombia. Central banks from India to Chile will set interest rates.

Asia

China’s PMIs, due Sunday, will dominate the start of the week as policymakers, investors and analysts try to gauge the current strength of the world’s second-largest economy.

Activity in the factory sector is forecast to return to expansion for the first time since September, while growth in the services sector is seen maintaining largely the same pace as in February.

"chart")

The Caixin manufacturing gauge the following day is seen showing a smaller expansion in its measure of activity that focuses more on the private sector.

PMIs from economies throughout the Asia-Pacific region the same day will give a feel for the regional growth outlook.

The Bank of Japan’s quarterly Tankan survey will probably reflect a continuing divergence in sentiment by industry. The gauge for large manufacturers is seen slipping for the first time in a year, while the reading for large non-manufacturers may soar to a 32-year high.

Smaller firms will likely be pessimistic, an outcome that could jeopardize wage gains at SMEs needed to power the virtuous cycle sought by the BOJ.

"chart")

South Korean export growth is forecast to cool in March, while consumer inflation data out Tuesday probably eased a tick there.

Price gains may speed up moderately in Indonesia and the Philippines. Declines in Thai prices are predicted to ease.

The Reserve Bank of Australia releases minutes from its March meeting on Tuesday, with two board members due to speak during the week. The Reserve Bank of India is expected to keep its main policy rates steady on Friday.

Europe, Middle East, Africa

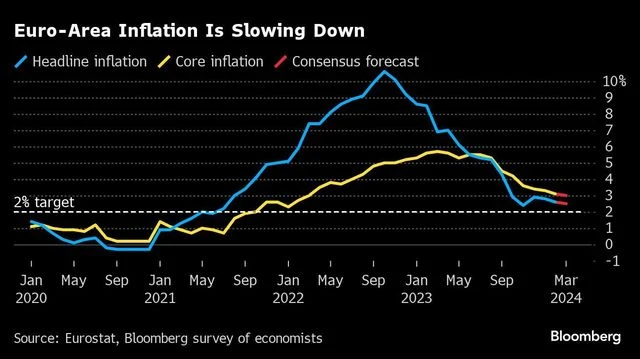

After last week’s consumer-price reports from France, Italy and Spain, and following a region-wide holiday on Monday, further puzzle pieces will emerge revealing the strength, or otherwise, of euro-area pressures.

German inflation on Tuesday is anticipated to show further weakening toward the 2 per cent target. The European Central Bank will unveil its survey of consumer expectations the same day.

The euro-zone inflation number will be published on Wednesday. Outcomes anticipated by economists at 2.5 per cent — and 3 per cent for the underlying gauge that strips out volatile energy and food items — may keep officials only inching toward cutting rates in the coming months as they gauge how their policy is constricting growth.

"chart")

Governing Council members have until the end of day Wednesday to share their views before a blackout period kicks in ahead of their April 11 decision. Further clues about their thinking may emerge the following day, when an account of their last meeting is published.

On Thursday, Sweden’s Riksbank will release minutes of its March decision, shedding light on an outcome that saw officials firm up plans to cut rates at some point in the second quarter.

Switzerland will release inflation numbers on Thursday. While an acceleration is expected, if it comes in as forecast at 1.4 per cent that would still be well below the ceiling targeted by the Swiss National Bank, which recently cut rates.

And in Turkey, where the central bank has been aggressively tightening, data on Wednesday may show another acceleration in consumer-price growth toward 70 per cent.

And in Turkey, where the central bank has been aggressively tightening, data on Wednesday may show another acceleration in consumer-price growth toward 70 per cent.

Several monetary meetings will take place this week in Europe and Africa:

- In Sierra Leone, with inflation still above 40 per cent, officials might be persuaded to raise borrowing costs again on Tuesday.

- The same day, Lesotho, which pegs its currency to the South African rand, may follow its neighbor and hold the key rate at 7.75 per cent to support its economy.

- In East Africa, Kenya’s monetary authority is also set to leave its benchmark on hold on Wednesday after a currency rally helped temper prices.

- Further east, Mauritian officials may hike borrowing costs after inflation hit an eight-month high amid recent heavy rains from tropical cyclones.

- Back to Europe, Poland’s central bank is poised to keep its benchmark at 5.75 per cent on Thursday against the backdrop of a standoff with the government.

- Romania’s central bank may consider the timing for its first rate cut after inflation started to ebb. That’s also on Thursday.

Latin America

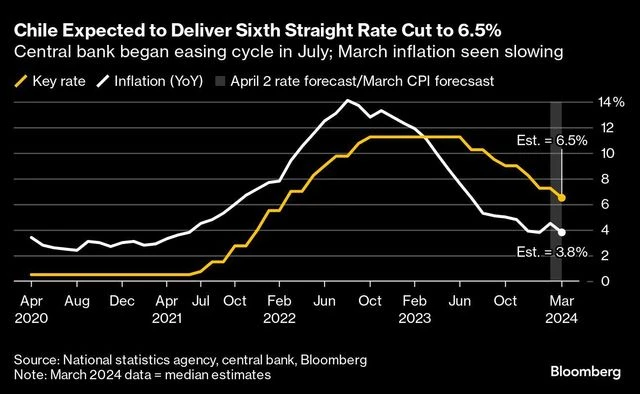

Chile on Monday posts February GDP-proxy data, likely cementing the view that its economy is on the rebound.

"chart")

The central bank on Tuesday is all but certain to trim borrowing costs for a sixth straight meeting, with an early consensus forecasting a 75 basis-point cut to 6.5 per cent, though an uptick in consumer prices and wobble in inflation expectations may put a smaller reduction in play.

Brazil releases a raft of data, including monthly trade, industrial production, current account, foreign direct investment and primary and nominal budget figures.

The week’s highlight in Mexico comes with the posting of the minutes of Banxico’s March 21 decision to cut the key rate to 11 per cent. While the post-meeting communique tilted hawkish, the minutes may push that vibe up a notch or two.

"chart")

Peru’s inflation data on Monday may show the annual print falling below 3 per cent, enough to persuade bank President Julio Velarde and colleagues to get back to cutting borrowing costs at their April 11 meeting.

Colombia’s central bank posts the minutes of its March 22 decision, when it doubled the pace of easing and lowered its rate to 12.25 per cent.

With March consumer price data on Friday expected to show a 12th straight month of disinflation, the odds are stacked in favor of another half-point move at BanRep’s April meeting.